Live Deal Review:

Personal Bank Statement File Review

Real-World Self-Employed Borrower Qualification Example

Before reviewing the income calculation, let's understand the borrower.

Borrower Profile

Borrower Type: Self-Employed Business Owner

Business Structure: LLC (50% Owner)

Business Age: 2 Years

Occupancy: Primary Residence

Loan Purpose: Purchase

Credit Score: 735

Borrower Snapshot

Challenge: Tax returns show significant deductions and insufficient qualifying income. He draws money from his business each month.

Objective:

Determine whether the borrower can qualify using Personal Bank Statements instead of tax returns.

Step 1: Identify

Many self-employed borrowers intentionally minimize taxable income through legitimate business deductions.

The result is often the same:

A financially successful borrower whose tax returns fail to reflect actual spending power.

In this case, the borrower deposits money each month from their business.

Personal bank statements could provide a more accurate picture of available income.

The challenge is documentation, not repayment ability.

Why Doesn't Traditional Financing Work?

Step 2: Structure

This can be especially useful when:

✓ Business structure involves multiple accounts and a lot of transfers

✓ The borrower owns 50% or less of the business

✓ Personal deposits clearly demonstrate income flow

✓ Tax returns do not accurately represent cash flow

The goal is to establish a consistent income stream using documented deposits.

What's the Best Qualification Strategy?

Personal Bank Statements offer a different option to calculate income without deducting expenses.

Business Bank Statements

Analyzes business deposits and applies business expense factors.

Personal Bank Statements

Analyzes deposits flowing directly into the borrower's personal accounts. Do not use expense factor unless used primarily as a business account.

Step 3: Validate

Before calculating income, verify the file meets basic eligibility requirements.

Personal Bank Statement Checklist

✓ Self-employment verified

✓ 12-months personal bank statements collected

✓ Verify that the names on the bank statements are on the loan

✓ Large deposits reviewed

✓ Transfers identified

✓ Reserve requirements confirmed

✓ Request 3-months of business bank statements

Once these items have been reviewed, income can be analyzed.

Income Calculation Walkthrough

Download the Personal Bank Statement to follow along or use your own calculations.

Step 1

Review total deposits and Identify any deposits that should not be included:

✓ Transfers between accounts

✓ Returned deposits

✓ One-time non-recurring deposits

✓ Funds that cannot be documented

The goal is to isolate the income deposits.

Download the calculator and follow along to use your own numbers.

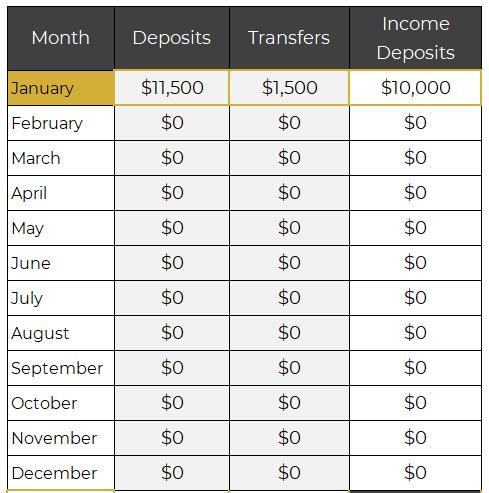

Start with total deposits shown on the Personal Bank Statements.

Our borrower has $11,500 in total deposits and $1,500 in transfers and returns.

Calculator Entries: Month 1

$11,500 monthly deposits

$1,500 monthly transfers

Results:

$10,000 income deposits

Step 2

Calculate the monthly deposits for the past year to get the full picture.

This provides the foundation for determining accurate monthly qualifying income.

Some business types have deposits that can fluctuate throughout the year.

Some months might be really high, while others can show no deposits at all.

Reviewing a full year will help to provide the most accurate annual income.

Review 12 Months of Bank Statements

Calculator Entries:

$11,500 monthly deposits

$1,500 monthly transfers

12 months total

Results:

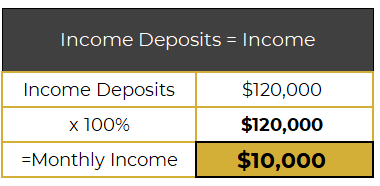

$138,000 total deposits

$18,000 ineligible

$120,000 income deposits

Borrower’s personal bank statements show $120,000

Step 3

Determine final monthly qualifying income.

Total income deposits are averaged over 12-months to get the monthly income.

There is no expense factor applied to personal bank statements as long as they have a separate business account established for their normal operating account.

If they are using the personal account as their business account, an expense factor must be applied in the same way as the business bank statement review.

Calculate monthly income for the loan.

Calculator Entries:

None required, Calculator does the work.

Results:

Total Income Deposits - $120,000

Personal Income - $120,000 annually

$10,000 Monthly Income

$120,000 / 12 months

Common Loan Officer Mistakes

⚠ Double-counting transfers

⚠ Including one-time deposits

⚠ Failing to identify undocumented funds

⚠ Failing to verify the existence of a business account

⚠ Assuming every deposit represents income

⚠ Overlooking reserve requirements

The strongest files are built around documented, recurring cash flow.

Outcome

Why This Structure Worked:

The borrower had strong cash flow but insufficient taxable income.

Personal Bank Statements provided a more accurate representation of the borrower's financial strength.

By reviewing recurring deposits and eliminating ineligible funds, a reliable monthly income was established and the borrower qualified successfully.

The solution wasn't finding a new borrower.

The solution was documenting the borrower's income differently.

Key Lessons

✓ Personal Bank Statements focus on deposits flowing to the borrower personally.

✓ Not every deposit represents qualifying income.

✓ Transfers must be identified and excluded.

✓ Consistency matters more than isolated large deposits.

✓ Strong documentation creates cleaner approvals.

✓ Personal Bank Statements can provide excellent solutions for self-employed borrowers whose tax returns understate actual cash flow.

Framework Review

Identify

Tax returns did not support qualification.

Structure

Personal Bank Statements selected.

Validate

Borrower and documentation requirements confirmed.

Calculate

Income determined using recurring personal deposits.

Outcome

Borrower qualified using documented personal cash flow.

Notice how the Non-QM Gold Framework was applied: