Live Deal Review:

Asset Depletion File Review

Real-World Asset-Based Qualification Example

Borrower Snapshot

Before reviewing the calculation, let's understand the borrower.

Borrower Profile

Borrower Type: Retired Executive

Employment Status: Retired

Occupancy: Primary Residence

Loan Purpose: Refinance

Credit Score: 760

Challenge: Limited employment income despite substantial liquid assets.

Objective:

Determine whether the borrower can qualify using Asset Depletion instead of traditional employment income.

Many financially strong borrowers no longer receive traditional employment income.

Retirees, semi-retired borrowers, business owners who have sold their companies, and high-net-worth individuals often have significant assets but limited monthly income.

Traditional underwriting may struggle to document sufficient qualifying income despite substantial financial strength.

The challenge is not the borrower's ability to repay.

The challenge is how that repayment ability is documented.

Why Doesn't Traditional Financing Work?

Step 1: Identify

Step 2: Structure

What's the Best Qualification Strategy?

Rather than relying on tax returns, we'll evaluate the borrower's eligible assets.

Asset Depletion programs convert qualifying assets into a monthly income stream for mortgage qualification purposes.

This approach is commonly used for:

✓ Retirees

✓ High-net-worth borrowers

✓ Semi-retired individuals

✓ Borrowers living primarily from investments

✓ Borrowers between careers

The goal is to determine whether existing assets can reasonably support the proposed mortgage obligation.

Coaching Note:

Many loan officers assume a borrower needs employment income to qualify. Asset Depletion often proves otherwise.

Step 3: Validate

Asset Depletion Checklist

✓ Asset statements collected

✓ Asset seasoning verified

✓ Eligible asset types confirmed

✓ Required reserves reviewed

✓ Property eligibility confirmed

✓ Credit profile reviewed

✓ Asset ownership verified

✓ Lender-specific depletion methodology confirmed

Once eligibility is verified, the income calculation can begin.

Before calculating income, verify the assets meet the program requirements.

Income Calculation Walkthrough

Download the Personal Bank Statement to follow along or use your own calculations.

Step 1

Begin by identifying the type of accounts along with the current balances.

Examples may include:

✓ Checking accounts

✓ Savings accounts

✓ Money market accounts

✓ Stocks and bonds

✓ Retirement accounts

✓ Investment accounts

Download the Asset Depletion Calculator and follow along.

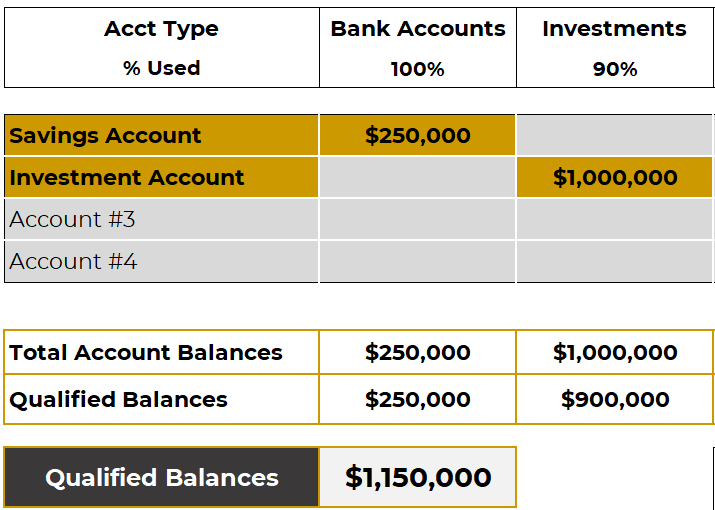

Calculator Entries:

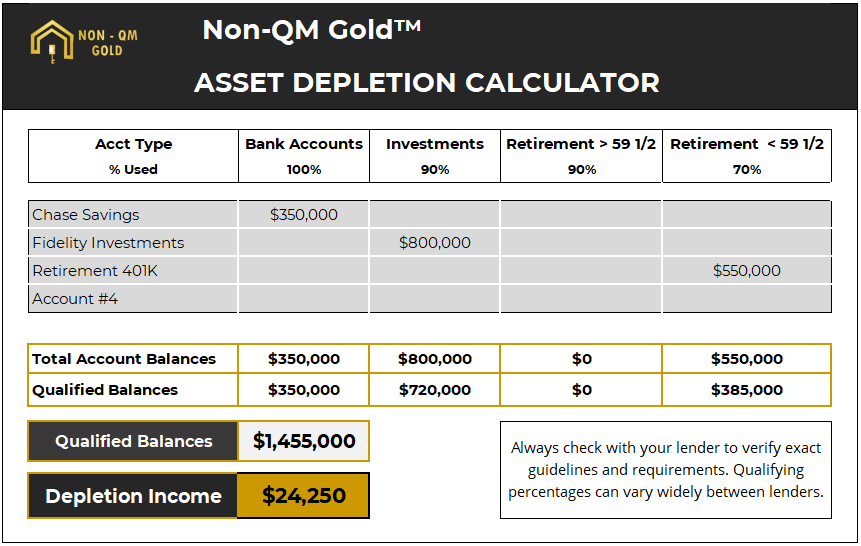

Savings - $250,000

Enter in Bank Accounts column

Investments - $1,000,000

Enter in Investments column

Results:

$1,250,000 in total current balances

$250,000 + $1,000,000 = $1,250,000

Step 2

Determine the adjusted qualified assets.

This step determines the total amount that can be used to calculate monthly asset depletion income.

Lenders do not always allow 100% of every account.

Example guidelines:

Bank Accounts: - 100%

Investment Accounts: - 90%

Retirement Accounts: - 70% if borrower is 59½+

65% if younger

These adjustments account for volatility and access restrictions.

Enter the balances into the correct column of the calculator.

The calculator does the work for you.

Calculator Entries:

None

Results:

Savings - $250,000 × 100%

= $250,000 qualified balance

Investment Account - $1,000,000 × 90%

= $900,000 qualified balance

Total Qualified Assets - $1,150,000

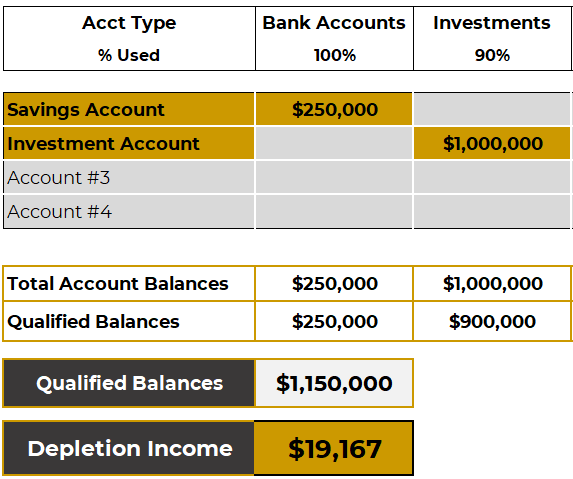

Step 3

Apply the lender's depletion period.

Asset depletion programs divide qualified assets over a specified number of months to create qualifying income.

Many lenders will use 60-months for the depletion period, but each lender can have different parameters.

The resulting figure becomes the borrower's monthly qualifying income.

This income can be added to other income types, such as W2 or bank statements.

Convert Assets Into Income

This is where the magic happens. Qualified assets are spread over: 60 months (5 years) and converted into income.

Calculator Entries:

None required- Calculation is instant.

Results:

Monthly Qualifying Income: - $19,167/month

$1,150,000 ÷ 60 months

Common Loan Officer Mistakes

⚠ Including ineligible assets

⚠ Using outdated asset statements

⚠ Missing lender-specific qualified percentages

⚠ Overlooking reserve requirements

⚠ Failing to verify ownership

⚠ Using the wrong depletion period

Many Asset Depletion issues result from guideline misunderstandings rather than borrower weaknesses.

Outcome

Why This Structure Worked:

The borrower had significant financial strength but limited traditional income.

Rather than forcing the borrower into an employment-based qualification model,

Asset Depletion allowed us to evaluate the resources already available to support the mortgage.

The result was a clear, defensible income calculation based on documented assets.

The borrower didn't need more income.

The borrower needed a different qualification strategy.

Key Lessons

✓ Asset-rich borrowers are often overlooked opportunities.

✓ Employment income is not always required.

✓ Asset Depletion converts assets into qualifying income.

✓ Different lenders use different depletion methodologies.

✓ Asset validation is just as important as income validation.

✓ Strong assets can create a very clean path to approval.

Framework Review

Identify

Traditional income was insufficient.

Structure

Asset Depletion selected.

Validate

Eligible assets and program requirements confirmed.

Calculate

Qualifying income created using lender-approved asset depletion methodology.

Outcome

Borrower qualified using accumulated wealth rather than employment income.

Before moving to the next scenario, notice how the Non-QM Gold Framework was applied: